Let's face it, owning and operating your own business will continuously pose opportunities, challenges, and risks. Product, service, people . . . each poses inherent variables that even with your best intentions can go sideways. As your business grows, adding a variation of what your business offers in the form of service or product can also introduce more risk as you scale. Even if 9 out of 10 things go well for your business, that one that doesn't can prove very costly.

General liability insurance helps to protect your business from a variety of risks, including injury to customers, customer property damage, and even advertising injury. While keeping your business protected from the high expense of lawsuits, there are some other benefits, including helping you to qualify for leases and contracts with the protection these policies provide.

As with any business expense, you will want to know ways to control costs, even if it means finding out more about this type of insurance. That's why Insurance For Texans looks to educate you whether you are a client or not. The more informed you are, the better choices you make as an insured. The better choices you make as an insured, the better the options you have from insurance carriers. The better options you have from insurance carriers, the better it is for a local, independent insurance agency to help you find those options for coverage.

What is General Liability Coverage?

Before we can talk about how to save money on general liability insurance premiums, we probably need to talk about what your general liability policy does. General liability is a business insurance policy that is like the Swiss Army knife of business insurance coverage. It's versatile and covers a range of incidents that could occur during the course of your business operations. Think of it like this: if someone slips and falls in your store, or if you accidentally damage a customer's property while conducting business, general liability coverage is there to help you handle the financial repercussions. It's not just about accidents, though; this coverage also helps protect you against claims of slander and libel. Yep, even words can land business owners in hot water these days!

In Texas, where businesses range from oil rigs to tech startups, having general liability coverage isn't just smart – it's essential. This coverage is tailored to meet the unique risks that come with running a business in the Lone Star State. So, whether you're slinging barbecue in Austin or running a boutique in Dallas, make sure your business is as protected as the Alamo – with robust general liability coverage. Remember, it's not just insurance; it's peace of mind in a state where business dreams grow as big as the Texas sky.

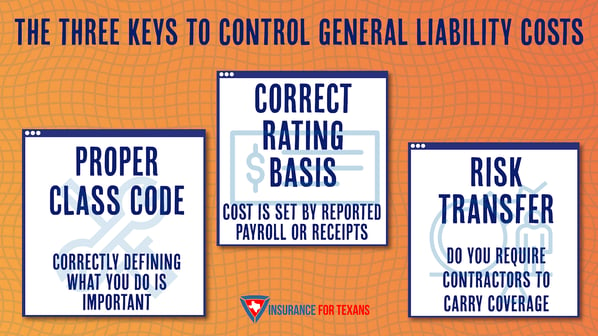

Three Keys To Controlling The Average Cost of General Liability For Your Texas Business

When it comes to controlling business insurance costs, you need to understand what drives them. Many business owners guess what decisions insurance companies make about how to calculate the price of commercial insurance policies. But we are sad to say that most guesses are not on target. It's probably the biggest hurdle that commercial insurance agents face regularly. Since everyone wants to know their cost of business insurance, let's take a look at some ways to control general liability costs.

Proper Class Code

The first thing that the insurance provider is going to do is determine what type of business that you are operating. It would make sense to do this since there is a different risk profile between a donut shop and giant manufacturing plant. As a result, correctly defining what you do when contracting for a general liability insurance policy is important to make certain your carrier knows how to correctly classify your types of risk that you encounter. If you have complex day to day operations your insurance provider needs to know that. General liability class codes are used by insurance carriers to assign a rating to particular businesses and industries related to the risk of the type of work done. Make sure that your commercial independent insurance agent has a strong grasp of everything that you do so that you business insurance premiums are rated correctly.

Correct Rating Basis

Once we have the proper class code, the insurance company is going to have to determine a way to put a level of risk to your business. This is typically done by using either annual payroll or receipts as a way to know how big your risk profile is with respect to business insurance rates. The easiest way to understand this is that you will have more business liability customers as the payroll or receipts climb. Both of these tend to bring more risk in the form of the likelihood of a claim or claims.

If you have more than one type of operation in your business, make sure that you are correctly grouping related to payroll or receipts to the type of operation. This will make sure that the size of your class code that was assigned for each type of business operation is appropriate to your biggest risk. You will also want to provide other helpful information, including (but not limited to) company payroll, gross sales receipts, size of your property, and the number of employees. When you think about class code and size basis together in determining annual premiums, it allows your guesses to make more sense.

Risk Transfer

The final piece that business owners can control costs of general liability risks is how they transfer risk to other people. Do you require contractors to carry their own insurance? Many businesses will utilize contractors, sub-contractors, vendors, and other service providers to conduct business in an efficient and cost-effective way. But adding other businesses into the mix of your business, you increase your exposure to risk. And every time we increase the risk exposure to your business, your liability premium will increase.

Requiring these contractors, sub-contractors, vendor, and other service providers transfers risk off of your business and places the liability where it belongs. This is a strategy that could prevent you from taking on the high costs of legal expenses if a customer incurs injury or damage resulting from the negligence of the service provider. Requiring general liability insurance from your contractors and sub-contractors should be considered a standard business practice and indicative of doing business with reputable business owners.

How Can I Get Help WIth General Liability Insurance?

We always recommend working with an experienced, independent commercial insurance agent when evaluating types of coverage, coverage options, and coverage limits. The experience of the insurance experts will allow you to have the right types of business insurance with the best insurance costs possible. At Insurance For Texans, our independent agents specialize in working with Texas business owners like yourself to get you the right types of protection for your future. You can call us at 469.789.0220 or click the button below to get started with controlling your general liability insurance costs.