I grew up as a Baptist preacher's kid in the Texas Panhandle, so I've spent most of my life in and around churches. One thing I've learned is that the real work of a church rarely happens during Sunday morning church services.

It happens on Tuesday afternoons when volunteers are packing food boxes.

It happens on Thursday evenings when families stop by looking for help.

It happens when a church opens its doors and decides to serve its community.

That's exactly what I saw when I visited Matt's church in Amarillo.

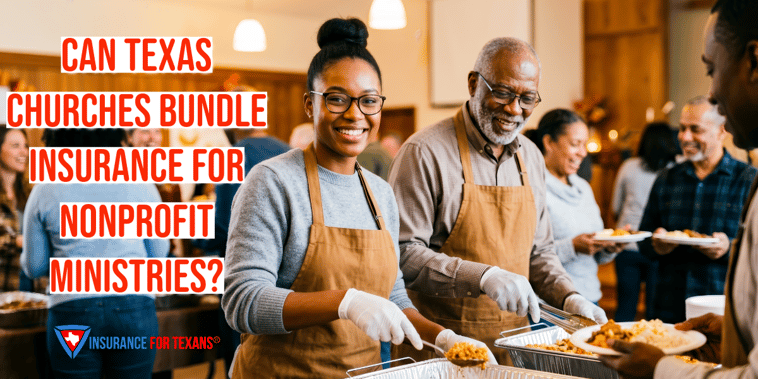

Matt was proud of what their congregation had built, and he should have been. As we walked through the building, he showed me room after room that had been transformed into ministry space. The old fellowship hall was now a busy food pantry. Former Sunday School classrooms had become a clothing closet filled with coats, shoes, and racks of donated clothes. Volunteers were moving everywhere, stocking shelves and helping families.

"We're helping dozens of families every week," Matt told me. "This is exactly why we're here."

I couldn't agree more.

But standing there watching all that activity, another thought crossed my mind.

I asked him a question that immediately stopped him in his tracks.

"Matt, how is all of this covered by nonprofit liability insurance?"

The smile disappeared.

He looked at me for a second and finally admitted, "Honestly, Ron, I don't know."

And that's when I realized we had a bigger conversation to have.

Does A Church Insurance Policy Automatically Extend to Ministries?

Like many church leaders, Matt had spent years thinking about ministry, volunteers, outreach, and serving people. He had never spent much time thinking about liability or the legal costs associated with a potential lawsuit. He assumed that because the food pantry and clothing ministry were church programs, the church's liability insurance automatically covered everything.

Unfortunately, that's not always true.

A volunteer gets hurt lifting boxes. A visitor slips and falls in the pantry. Someone claims food distributed by the ministry made them sick. Suddenly, what started as a ministry opportunity becomes a liability claim.

Matt wasn't careless. He was doing what most church leaders do. He was focused on serving people.

The problem is that insurance companies don't look at ministry the same way churches do.

And if your church is operating multiple outreach programs, food pantries, clothing closets, counseling ministries, or community service projects, understanding how those activities affect your insurance coverage has never been more important.

Why Are Church Insurance Policies Changing?

Matt's situation is becoming the new normal for churches all across Texas. As congregations rightly expand their outreach to meet the needs of their communities, they are unintentionally walking into a minefield of liability.

The problem is that many insurance policies were written for a time when "church" meant Sunday services that take place in the worship center and a Wednesday night potlucks in the fellowship hall. They weren't designed for a world where churches operate food banks, clothes closets, daycare centers, counseling services or addiction recovery on church property.

Insurance carriers have been hit hard by massive losses from Texas weather and are now looking at every policy with a magnifying glass. They are tightening their definitions of what "ministry" is, and anything that looks like a separate, specialized operation can be excluded if it’s not explicitly addressed.

This leaves well-meaning churches like Matt’s dangerously exposed that think they’re covered, but are actually one accident away from a financial catastrophe.

Are The Separate Nonprofits In Our Church Covered By Our Policy?

It's highly unlikely. If your community ministry operates as a separate legal entity, it is likely not covered by your church’s standard insurance policy. This is true even if it's housed in your church building. Each ministry needs its own specific protection.

For good legal and financial reasons, many churches structure their larger ministries as separate 501(c)(3) nonprofit organizations. This is common for food pantries, daycare centers, or schools that operate under the church's umbrella.

The critical mistake happens when the church assumes that their general liability insurance automatically extends to each separate entity. From an insurer's perspective, they are separate organizations.

Think about it this way: the "Named Insured" on your church's policy is the church itself. If a lawsuit names the food pantry, and the food pantry is its own legal entity, the insurance company for the church will deny the claim.

They have no legal obligation to defend an organization that isn't on the policy. This is the kind of fine-print detail that can lead to disaster. For Matt’s Amarillo church, if their food pantry is its own nonprofit, a claim against the pantry would be denied. This would force the church to pay for legal defense and any settlements out of its own pocket.

How Does Community Engagement Increase Our Church's Liability Risk?

Anytime you invite the public gatherings onto church property or interact with them through ministry, you increase your church's exposure to liability claims. More people and more activities simply create opportunities for things to go wrong.

The moment you open your doors for a community program, you’re taking on new risks. General Liability insurance is designed to protect your church from claims of bodily injury or property damage. Most people think of the classic "slip and fall" scenario, like a visitor tripping on a cracked sidewalk in the parking lot. But for a church like Matt’s, the risks are much broader.

Consider the food pantry. What happens if a volunteer slips on a spilled can of beans and breaks an arm? What if a family claims they got sick from donated food? Or what about the clothes closet? A rack could tip over and injure someone, or a volunteer could be accused of wrongdoing.

Each of these scenarios can trigger a lawsuit. Without the right coverage, the legal expenses alone could be devastating, even if the church is ultimately found innocent. The more you serve the community, the more you need to be absolutely certain your liability coverage extends to these activities.

Can We Bundle Liability Coverage For Our Church And Its Ministries?

Yes, you can and absolutely should bundle the coverage for your church and its ministries. A great agent will ask detailed questions about your operations before ever giving you an insurance quote. During this conversation, you need to fully disclose all of your church’s ministry activities.

The best and most affordable way to handle this is to have a single, comprehensive policy that covers both the church and its specific outreach activities. This can't be done with a cookie-cutter approach. It requires an agent who takes the time to understand exactly what your church does. This is where the philosophy of the agent you work with becomes critical.

A lazy agent will focus on insurance costs and just ask for your building size in order to spit out an insurance premium number. They won’t ask about the food pantry, the clothes closet, or the youth mission trips. As a result, they are selling a piece of paper, not real liability insurance protection.

Our True Texas Church Insurance agents start with questions, not generic insurance quotes.

- Are your ministries separate legal entities?

- How many volunteers do you have, and how are they screened?

- Do you transport people in church-owned vehicles?

- Are the vehicles protected by commercial auto insurance?

- What activities do you run, and who do you serve?

This conversation is essential. By disclosing all your operations, an independent Texas church insurance agent can work with carriers to craft a single policy that specifically names and covers your church AND its nonprofit ministries. This closes the dangerous gaps and often results in a better value than trying to patch together separate, conflicting policies. It transforms your insurance from a source of anxiety into a tool that empowers your ministry.

How Do We Make Sure Each Ministry is Covered?

For Matt, that conversation was a wake-up call. The anxiety he felt was real, but it was also the first step toward true peace of mind. We sat down and discussed the church's coverage options.

- First, review your structure. Do you have separate nonprofits operating within your church? If so, gather the legal paperwork. You need to know exactly who owns and operates each ministry.

- Second, document all your activities. Make a list of every single outreach program, from the weekly food pantry to the one-time summer youth camp. Don't leave anything out.

- Third, have an honest conversation with an insurance agent who specializes in church insurance. Show them your list. Explain how you operate. If the agent isn't asking you clarifying questions, it should terrify you. They are not the right agent for your church. You need a partner who is as dedicated to protecting your church and ministries as you work to grow them.

True Texas Church Insurance

You shouldn't have to be an insurance expert to lead a church. Your calling is to serve your community and share your faith, not to spend sleepless nights worrying about liability loopholes and policy exclusions.

That’s our job.

At Insurance For Texans, we don’t believe in one-size-fits-all solutions. We believe in taking the time to understand your unique Texas church. Our True Texas Church Insurance program begins with a personalized risk assessment. We dive deep into your operations to ensure every aspect of your mission is protected.

If you’re ready to stop guessing and get clarity on your church’s protection, let’s schedule a conversation. Our church insurance agents have worked with hundreds of Texas churches to build a plan that safeguards each church’s mission.

Click the button below to get started today.