Marcus is the kind of guy who keeps his home in Lubbock in tip-top shape. He has lived in the Hub City for years and knows that when those West Texas winds start howling, you better have your property secured. He stays on top of his home maintenance like a hawk, making sure his filters are changed and his yard is tidy.

When a standard storm rolled through last spring, Marcus did not panic because he knew he had a replacement cost policy with one of the major home insurance companies. He figured that as long as he paid his insurance premiums on time, his insurance policy would be there to catch him if he had hail damage.

He called one of his local roofing contractors to come out for a damage evaluation after the golf ball sized hail stopped bouncing off his porch. The roofing material was clearly beat up, with obvious granule loss and bruised asphalt shingles that were not going to survive another season of South Plains sun. Marcus felt confident as he started the insurance claim process, expecting a smooth path to a roof replacement.

The conflict started when the insurance company adjusters showed up with a different story. Despite clear hail impacts on his shingles and roof vents, Marcus received an insurance settlement offer that was barely enough to cover a minor roof repair. He found himself staring at a massive bill because his policy was riddled with hidden traps designed to protect the carrier's bottom line rather than his home.

Marcus learned the hard way that the standard homeowners insurance of five years ago has been replaced by a system that leaves you holding the bag.

Why Is This Happening to So Many Texas Homeowners?

Marcus's story is the new reality for property owners across Texas. We live in a part of the country often referred to as Hail Alley. The frequency of severe weather has pushed insurance companies to their breaking point.

Every year, hail storm damage insurance claims rack up billions of dollars in losses and it is the single biggest driver of premium increases for Texas Home Insurance.

To keep their own costs down, the big corporate insurance carriers are shifting the financial burden of hail damage claims back onto you. They are no longer offering the replacement cost dwelling protection we are used to.

Instead, they are using complex exclusions and fine print to limit their exposure. Homeowners are not finding out about these changes until there is roof damage and they are already deep into the process with their claims adjuster. Your coverage limits are evaporating a little more every year, and it is happening right under your nose.

The 5 Roof Replacement Traps Waiting to Trip You Up

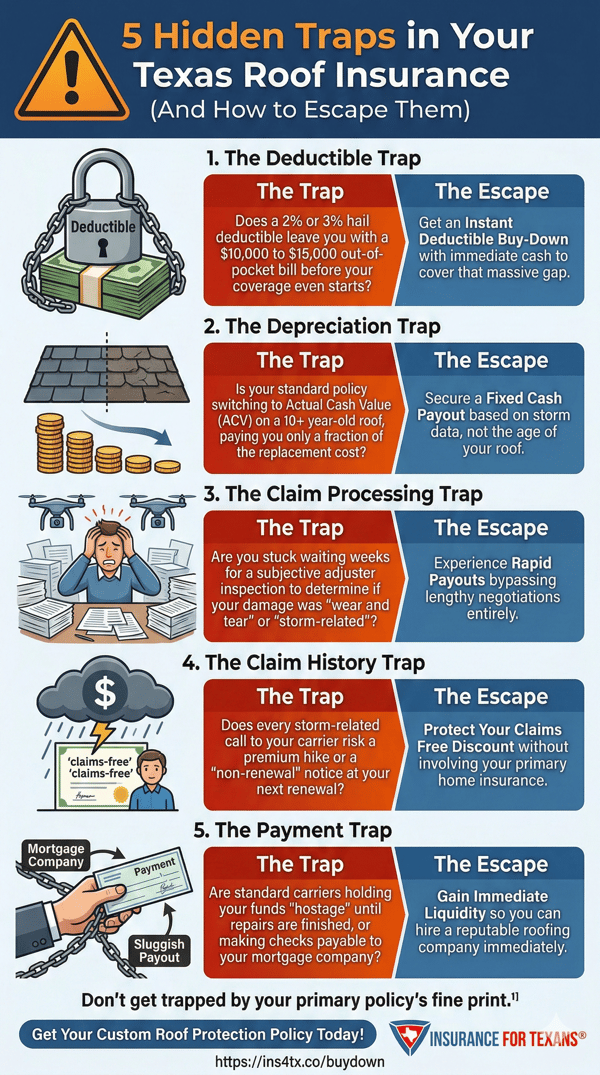

1. The Deductible Trap

Texas home insurance policies have moved away from flat dollar amounts long ago and use percentage deductibles for wind and hail. If your dwelling coverage is $500,000 and you have a 3% deductible, you are on the hook for the first $15,000 or roof repair or replacement. That is a massive out-of-pocket barrier that stands between you and a safe home.

2. The Depreciation Trap

As your roof's lifespan moves past the ten-year mark, many home insurance companies switch you to a roof payment schedule that pays only for the actual cash value of the old shingles. You might have recoverable depreciation in your head since old replacement cost policies had that available. But the reality is often a check for "garage sale prices" that does not even come close to covering the replacement of modern roofing material costs.

3. The Claim Processing Trap

The hail insurance claim process has become a gauntlet of inspection report disagreements from roof inspectors. You might be forced to deal with storm date attribution disputes where the carrier claims the damage happened years ago based on granule loss. Waiting on a sluggish adjuster can leave your home vulnerable to leaks while you fight over the claim documentation.

4. The Claim History Trap

Even if you just call to ask a question after a roof inspection or damage evaluation, it can show up on your claim history record. Filing a small roof insurance claim can lead to a massive hike in your insurance premiums at your next renewal. In some cases, carriers are using claim documentation to issue non-renewal notices to homeowners in hail-prone regions.

5. The Payment Trap

When you finally get an insurance settlement for a hail claim, the check is often made out to you and your mortgage company. This creates a massive delay in getting the funds to your roofing contractors for work to get started. If you lack the liquidity to act fast, it leaves your home and other structures coverage at risk while you wait for the bank to release your money.

How Can You Get Your Hands on an Instant Hail Buffer?

Fortunately, there is a new way to handle these claims without insurance disputes. You need a solution that covers the gaps left by your primary home insurance policy. True Texas Home Insurance has a standalone hail insurance product that acts as the "Texas Hail Buffer."

This is not a traditional homeowners insurance policy. It is a specialized tool that provides a flat cash payout based on meteorological data from the National Weather Service and simple visual damage documentation. You do not have to wait for insurance company adjusters to argue about granule loss or the age of your roofing material.

This coverage sits right alongside your existing dwelling protection and pays out up to $25,000 to cover hail damage or violent wind storms. Because it is a policy for roof damage from a separate insurance company, it does not touch your claim history. This can allow you to keep your "claims-free" status while getting the money you need for a roof replacement or repair.

Are You Ready to Take the Guesswork Out of Your Protection?

The payout on these claims happens fast, usually within two weeks of the damage from hail impacts. This gives you the cash to hire a professional roofing contractor on your own and get your materials ordered before the next round of weather hits. It removes the stress of worrying if you will get recoverable depreciation or a denial letter.

Whether you have traditional shingles or Impact-Resistant Roofing Materials, this inexpensive addition to your homeowners insurance provides the clarity you deserve. It is about knowing exactly how much cash will be in your hand when the sky starts falling.

This is the heart of our True Texas Home Insurance program. To make sure you are not blindsided by the fine print of Insurance Regulations and policy jargon.

We want you to stop guessing and start knowing exactly where you stand. You deserve peace of mind knowing your financial future is protected from the unpredictable nature of Texas weather.

We have seen too many people like Marcus get caught in these traps, and we are here to make sure you have the escape hatch ready.

Click the button below to get your own special roof protection policy today!