Retiring early is a dream for many Texans. Since the COVID lockdowns of 2020 and the subsequent craziness in the employment market, the number of couples that are close to the retirement finish line considering leaving the workplace has exploded. The headaches associated with return to offices, demands on time, and just general malaise of the workplace politics has led many of us to rethink what we really need in life. And time with our families and friends seems a lot more important to us which is leading to many choosing early retirement even if it's not quite as glamorous as we might have dreamed it.

Congrats to those who have prepared for this days and can now enjoy it. But losing access to the employer-sponsored health insurance that typically comes with full-time employment, how do you get access to affordable health care coverage? For our friends Joseph and Nadine, they began to look at health insurance options and that simply made their heads spin due to the complexity and obfuscation of what exactly was offered in the current Texas health insurance marketplace. Not only are there different mechanisms to obtain health insurance coverage, but the options inside those mechanisms seems to be endless.

But we have great news! Just like we did for Joseph and Nadine, Insurance for Texans has created a formula which can help you determine not only which mechanisms that you can consider. But also how to parse through the endless options available inside those mechanisms.

Questions To Answer For Early Retiree Health Insurance

When we sat down with our friends Joseph and Nadine, they informed us their upcoming date to walk away from working. We celebrated with them and began asking questions about how they were going to cover their health insurance. Before anyone can make a recommendation to you, they have to know what your specific situation will be. The couple had been on Joseph's health plan from his employer for as long as they could remember, which was a really benefit rich plan. And while they absolutely could keep that plan using COBRA Coverage, since they were both 61 years old they couldn't keep the plan all the way to that 65th birthday when they could enroll in Medicare. So what questions should you be considering before you chart a path to obtaining health insurance as an early retiree.

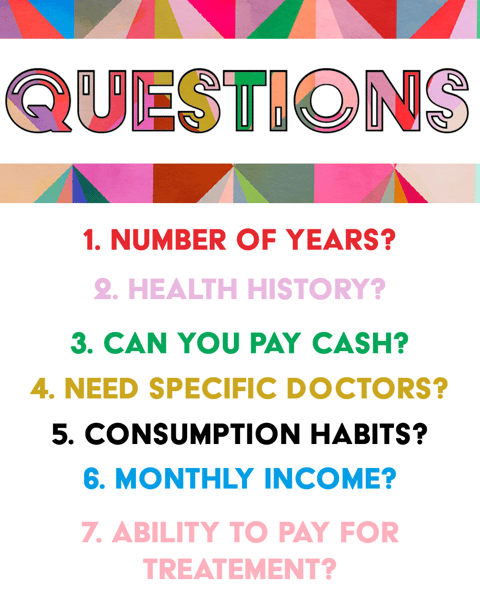

Here are our First Seven Questions that we asked Joseph and Nadine as they faced this task.

- How many years will you need to cover with an individual health insurance plan?

- What does your health history look like?

- Are you comfortable paying cash for a doctor's visit, prescription, or test rather than using insurance?

- Do you have specific doctors or treatment locations that _MUST_ be available to you?

- How much health care do you consume on an regular basis?

- What is your monthly income going to look like post retirement date?

- How much free cash flow do you have to throw at a health scenario that requires either large or continuing treatment?

The Insurance for Texans agent definitely probed beyond these seven questions so that we could provide consultative advice to our friend Joseph and Nadine, but the answers to these questions allowed us to begin to whittle away at which of the four key mechanisms of early retiree health insurance were available to them along with helping us make a solid recommendation that they could understand.

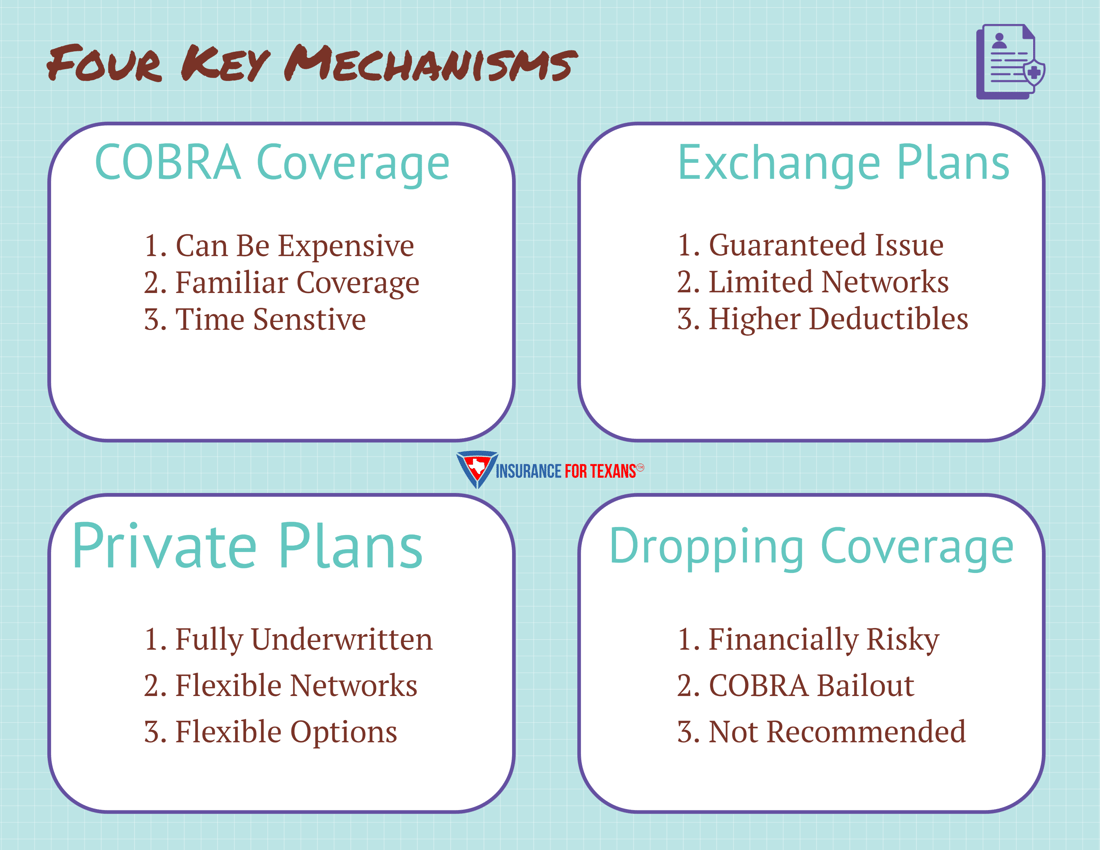

Four Key Mechanisms Of Early Retiree Health Insurance

In considering retirement, Joseph had been looking at information from different sources from the internet about what kind of health insurance was available to individuals. When comparing between the options between websites, it became obvious that some people were slanting their viewpoint based on what they wanted to sell to Joseph. But he remembered that his insurance agency was independent which meant that they can provide many solutions to their customers rather than just a preferred mechanism. Let's look at the four key mechanisms of coverage below.

One note on why we don't mention a fifth mechanism for you. Some folks consider health sharing plans as the fifth option for health coverage. Nadine actually asked us about a health sharing plan when we talked. While there are health sharing plans that do some great work for Texans, we have seen their pitfalls when people don't understand what they are and how they operate. We can definitely provide insight on these plans to you, but please remember first and foremost that they are not actually insurance and therefore are not regulated by the state department of insurance. That means if you have an issue with a reimbursement, you have to obtain your own lawyer and cannot leverage the complaint process that is afforded to you by the fine folks in Austin at the DOI.

With that said, let's look at the four mechanisms that Joseph and Nadine considered when looking at health coverage for the gap in coverage between the retirement date and when they could enroll in Medicare as part of their retirement benefits.

- COBRA Health Coverage

- ACA Marketplace Exchange Health Insurance Plans

- Private Individual Health Insurance Coverage

- Dropping Health Insurance Coverage Altogether For A Period Of Time

Details On The Four Mechanisms

1. COBRA Health Coverage

While Joseph worked at his job with a large international corporation, he was afforded great health insurance through a his monthly benefit package. The options available allowed he and Nadine to have very deep benefits while also keeping their medical expenses low since the cost of the coverage was heavily subsidized by his employer. The great news is that there is legislation that allows you to keep your employer based coverage when you leave active employment with them for up to eighteen months. That means that you can keep the medical costs low with that Cadillac coverage plan that you love.

The downside is that these plans can be very expensive and since your employer has been paying a large portion of your health insurance premiums it is very likely that you will have sticker shock when you realize just how much it actually costs out of your pocket each month. Along with this, if you are like Joseph and Nadine and need coverage for greater than eighteen months, it is not a long term solution for someone trying to get to the Medicare retiree health benefits.

2. ACA Marketplace Exchange Health Insurance Plans

The next health insurance mechanism that most early retirees take a look at are what are known as "Marketplace Plans", "Exchange Plans", "ACA Plans", or "Obamacare Plans". This mechanism is not a retiree health benefit in any way, but is a health insurance plan that can be issued through the Special Enrollment Period that comes with this life event called early retirement. The rules for these plans is governed through the Affordable Care Act and subsequent legislation that controls the administration of these plans.

The great news is that you cannot be denied coverage regardless of pre-existing conditions, chronic conditions, household size, or household income. It does not have a time bound on it like COBRA health plans and will be guaranteed renewable until age 65 when you enroll in Medicare.

The downside for these plans is two fold. First, is simple network access. Nadine had a doctor that she loves who did not accept this insurance plan which meant that she was going to either find a new doctor or pay cash to see the one she loved. Second, is that the out of pocket health care costs on these plans is usually fairly high. Deductibles of $5,000 plus is common. That means that you have to weigh the out of pocket costs against the monthly premium costs.

One other thing to consider with these plans when thinking about positives and negatives is that your household income, which is generally reduced from your working days, will affect your monthly premiums. The Affordable Care Act has provisions that allow for premium subsidy based on a sliding scale tied to income levels. This subsidy is regulated by the Internal Revenue Service through a Federal Income Tax credit that can be applied either in lump sum on your return or in monthly portions against the premium payment to free up cash flow. Since the subsidy is tied to income requirements and household size, knowing that the subsidy payments will be reconciled on your yearly income taxes understanding the implications of these calculations will be vitally important the success of managing your financial retirement benefits.

3. Private Individual Health Insurance Coverage

Some people choose to move into the private health insurance marketplace. These plans are fully underwritten and subject to preexisting conditions being able to exclude you or your spouse from coverage. Since Joseph had the chronic condition of Type 2 diabetes that was managed by medication we had to have a conversation around what that meant for them in this portion of the healthcare marketplace. There are typically three types of private individual medical insurance. Short Term Medical Plans, Catastrophic Health Plans, and Limited Benefit Health Plans.

Short Term Medical plans are governed by the Affordable Care Act are generally used to bridge gaps between enrollment periods or other coverage. That said, they are currently renewable for up to a three year time period and some health insurance will even guarantee up to the three year window of coverage. This makes them a viable option for retirees age 62 and above looking to lock in defined coverage during the gap time period. While the premiums can sometimes be considered expensive, they also typically provide an expanded network over some other options out there. Since our friend Joseph and Nadine were age 61, this wasn't considered a great option for them.

Catastrophic Health Plans are typically considered either very HIGH deductible plans or for the very young. But that's not the truth. There are plans available that will provide a very affordable deductible at say $1,000 per illness or accident, but will also not be involved in your day to day healthcare like an annual checkup to your PCP or prescriptions. You need to be prepared to cover some medical costs out of pocket. However, the premiums are typically considered very affordable which is what caught Joseph's eye during our conversation with them. These plans make a great mechanism to cover big events if you use a Direct Primary Care Physician or some other form of a cash pay doctor relationship.

Limited Benefit Health Plans are exactly what their name implies. They are not going to cover all of your healthcare related costs because there are limits! Duh! We typically don't recommend these as a stand alone way to obtain retiree coverage unless you have some really unique retirement benefits that make them monetarily viable. Because of their extremely low cost, having an indemnity plan to offset out of pocket costs or a cancer plan to cover expenses directly related to cancer treatments but not covered by your main health plan can make them great supplemental benefits which is why Nadine loved the idea due to family history.

The key to using these private health plans is understanding their limitations compared to your current coverage while also seeing them as potentially able to offer ancillary benefits or supplemental benefits to other forms of retiree insurance coverage.

4. Dropping Health Insurance Coverage Altogether For A Period Of Time

As much as we don't want to bring this up, we have seen some people who have soured on the cost of retiree coverage simply drop health coverage altogether. If you're simply a few months shy obtaining Medicare no longer under a plan that requires active employment we guess it could make sense. There is typically a 90 day window where COBRA coverage can be activated if a life event created a need for coverage. That said, if you're going more than a few weeks without continuous coverage, please reconsider your thought process. It can absolutely decimate your retirement benefits.

How To Make A Choice Prior To Retiring

Given the four key mechanisms mentioned above, Joseph and Nadine ultimately had to make a decision on how to obtain retiree health coverage prior to walking away from their jobs. To them, it was important to maintain access to preventive care services with limited out of pocket costs due to family history and the chronic condition that Joseph managed well with his physician. They decided that the cost for keeping their current coverage via COBRA was not a financially viable option for health insurance simply due to cost. However, using marketplace coverage along with a limited benefit indemnity plan to offset out of pocket health costs meant that they could have the retiree health coverage that they needed at a price they could afford.

If you would like to have an independent insurance agent help you navigate the options for health insurance that available for early retirees, let Insurance For Texans help you with creating a health benefit package that will bridge the gap to Medicare. We have access to multiple options in the four key mechanisms that make obtaining retiree insurance coverage affordable and effective. You can use the form below to start your journey or call us at 469.789.0220 today!