Many homes in Texas are purchased between Easter and Halloween. As a result, a lot of homeowner insurance policies come up for renewal during that time period. Insurance For Texans is fielding a lot of phone calls around renewals right now because of this, and Texans are looking for ways to save money on their Home Insurance. Many of these Texas homeowners ask the simple question of do higher deductibles really save money on my Texas Home Insurance. The answer is, but! Which always seems to be our answer.

When evaluating money saved, it requires a couple of different pieces of information. First and foremost, if you move from a 1% wind and hail deductible to a 2% wind and hail deductible for your home insurance, you will see immediate relief on the premiums you pay for the upcoming year. That is simply not debatable by any person with a rational mind. But since everyone in Texas is rational, let's look at this from a slightly different angle.

Typically speaking, the price differential on an annual premium for 1% deductible vs a 2% deductible for a home with a replacement cost of $250,000 is going to be anywhere from $100 to maybe $400. So what you've done is trade $2,500 in potential deductible payment for $100 to $400 in savings that first year. If you live in an area of Texas where hail is less prevalent, that may see like a great way to proceed. It is entirely likely that you could go five to ten years without a hail claim. If you life between Plano and The Red River where people get their roofs replace at least once a year it seems like. This could make a different story. Let's do some math. One of Ron's favorite things.

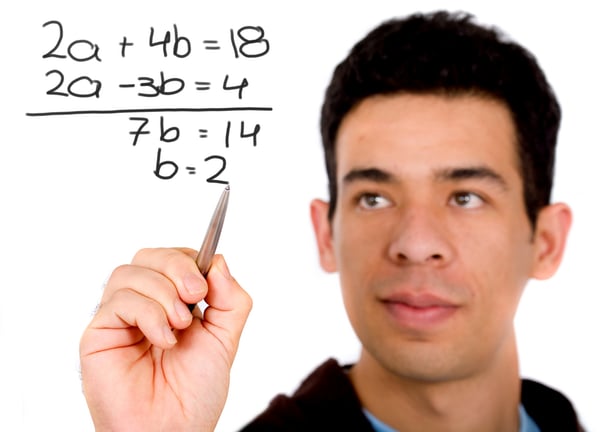

If you save $400 per year by moving from a 1% to a 2% deductible on that home with a $250,000 dwelling value, how many years would you have to be claim free to break even on the reduced premium? Well, 1% of $250,000 is $2,500, which is the amount of extra deductible you would be responsible for in the event of a claim. Doing some simple division of $2,5000 divided by $400, you would not break even on those $400 savings until year seven! And this assumes you get maximum savings of $400. The reality is that the average is more like $200 to $300. So now we are pushing that time horizon further out to break even. So Collin County residents really need to evaluate their homes are hit by hail and how likely they are to need to replace the roof due to hail to determine if this move actually saves money.

If you save $400 per year by moving from a 1% to a 2% deductible on that home with a $250,000 dwelling value, how many years would you have to be claim free to break even on the reduced premium? Well, 1% of $250,000 is $2,500, which is the amount of extra deductible you would be responsible for in the event of a claim. Doing some simple division of $2,5000 divided by $400, you would not break even on those $400 savings until year seven! And this assumes you get maximum savings of $400. The reality is that the average is more like $200 to $300. So now we are pushing that time horizon further out to break even. So Collin County residents really need to evaluate their homes are hit by hail and how likely they are to need to replace the roof due to hail to determine if this move actually saves money.

If you are looking at your Burleson Home Insurance options and not having discussions like this blog post about deductibles, maybe you should consider using a different agent. Insurance For Texans is a local Independent Insurance Agent that works for you and not some big corporation. Our professional agents work to make sure that you understand your options in the market place rather than trying to stuff you into a singular solution that only works for some. Speak with Tricia Conrad or Dena Davis today about how we can simplify and get you the best home insurance coverage for you at the best price.