Now that we are in between the two hail seasons that Texas has the good fortune to experience, insurance claims have shifted to problems other than hail damage in Texas homes. The winter especially provides opportunities like freezing pipes to burst or that pesky slow leak to finally reveal itself. And when that happens, Texans find out that the insurance companies often have more than one type of deductible on their homeowners policies. Which can create some confusion for people like Sarah who lives in Odessa.

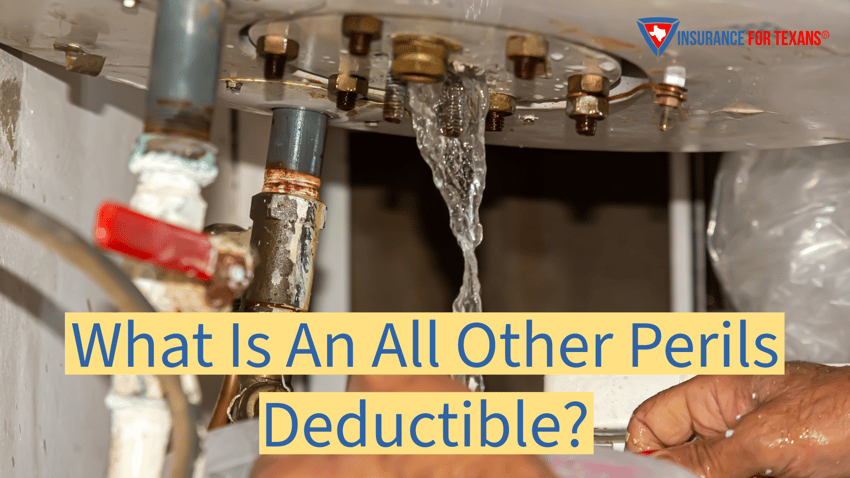

Sarah woke up to the sound of running water in her home and panicked as any of us would. If your house is like mine, it is designed to not have the sound of running water unless very specific activities are being engaged in. And we all know what kind of damage water can do to our homes! Sarah quickly determined that her hot water heater had decided that today was the day it was no longer in service. The drain faucet in the bottom had given way and water was now cascading through her house. Her first thought was to get the water shut off, which is what it should be. Once that was accomplished, she then began to rummage through her memory trying to remember what her homeowners insurance company was so that she could begin the claims process.

Fortunately for Sarah, all she had to do was call Insurance For Texans. Because we are an independent insurance agency we work with many home insurance companies, and we keep the details of not only the company that Sarah has coverage through, but also the type of insurance policy and the corresponding terms. Sarah was surprised that her homeowners policy had separate deductibles for storms and other covered claims. So we quickly walked her through the process of how her homeowners insurance claim would work and when she could expect claims payments to be made. But what about that pesky homeowners insurance deductible that is going to come out of Sarah's pocket?

Types of Deductibles

Standard Home Insurance Policies issued in the state of Texas have multiple deductible options available to you whether you live in Odessa like Sarah or in Grapevine or Houston. There is a special deductible for wind or hail storms, which is almost always a percent deductible. That means that you are responsible for an amount of money that is equal to the state percentage of your dwelling coverage amount on your home policy. Some people confuse what the percentage is applied against, so we wanted to make sure that we are clear.

Beyond that, there may also be a special deductible for tropical storms, also known as a hurricane deductible. Otherwise, every other covered claim by your homeowners policy is going to be subject to what is known as an "All Other Perils Deductible". If you are like Sarah, you are asking yourself or us, what exactly does that mean to you now that your home has water damage created by the water heater.

So What Is An All Other Perils Deductible?

While most people are familiar with the hail deductible on their homeowners insurance policies, they lack insight into much else simply due to the claim frequency from hail storms. But the other homeowners insurance deductible that is often overlooked, is the deductible named All Other Perils. This is a deductible that will be applied to all claims that are not covered by the wind, hail, tornado, and hurricane damage. So long as the damage to your home was created by a covered peril! The range of perils that your home policy covers are determined by the words in your contract, but the most common perils are going to be water, fire, theft, and other items named in the list of insurance perils. But if your policy is an open perils policy, it would cover anything not named in your exclusions list. That's a lot of words, but it's important to understand.

Unlike the wind deductible, the All Other Perils can be either a percentage deductible or flat dollar amount deductible. This greater flexibility is because this deductible is less likely to be used to commit fraud in the way that hail claims can be with deductibles. As a result, you will usually see options for the All Other Perils deductible set as low as $1,000. But you can also see them as a percentage of the dwelling coverage amount just like the wind and hail deductible. Because of this, all of your deductibles may be the same across the board even though the insurance provider gives you the ability to manipulate them separately.

And why do I care?

And why do I care?

When the independent insurance agents at Insurance For Texans discuss Ft Worth Home Insurance, deductibles are always a big part of the discussion. Most Texas homeowners get locked into worrying about what their wind and hail deductible is on their policy, and rightfully so. It is the most frequent type of claim that our clients deal with for their home. However, there are different kinds of deductibles on home insurance policies sold in Texas. And the one that allows you the most flexibility is the All Other Perils deductible.

The biggest type of claim that is filed in Texas for things not wind and hail related, is for water. This would be exactly what had Sarah in the claim situation for her home. These water claims can be nasty and run into the tens of thousands of dollars in unexpected repairs. Most of us have watched homeowners insurance premiums skyrocket over the last two years and knowing that we can lower our out of pocket expenses in a claim like Sarah's can be a great comfort knowing how all of this costing you and I today. If you decide to take a lower deductible, you can have these situations cleaned up for very little out of pocket.

But there is always a catch, right? As faithful readers of the Insurance For Texans blog know, there is no such thing as a free lunch. You must consider that as you lower the All Other Peril deductible, the premium payments will increase. You have to weigh the pros and cons of having a lower or higher deductible. It's a different answer for every family and for some the premium savings with a higher deductible amount is exactly what they are looking for. The great news for you is that TRUE Texas Home Insurance can help you navigate this decision while making sure that your coverage options do in fact provide the protection that you deserve.

Working with Insurance For Texans will give you the financial protection that you are craving from homeowners insurance policies. Since we work with many different companies, you will be able to compare policy to policy without the legwork of obtaining proposals from all of the different insurance providers.

If you want an advocate that works for you, and not some giant insurance company, click that button below or call us at 469.789.0220 today!